The Global Problem in Kenya's Tax Protests

The Global Problem in Kenya's Tax Protests

On the ongoing debt-servicing crisis, and how poorly it bodes for global readiness

While the West reels from yesterday’s most sensational SCOTUS decision, France’s far-right turn, Hurricane Beryl reaching Category 5 status through the Caribbean, and India processing a mass death by stampede—austerity protests continue in Kenya.

Maybe they’re not quite as exciting as everything else going on, to the rest of the world.

Indeed, many could even be excused for thinking the Kenyan issue a local affair.

But what Kenya is experiencing matters deeply, because it’s a perfect everyday example of things falling apart in ways with “cascade-failure” written all over them.

On the surface, there are the usual concrete factors and predictable players.

President William Ruto triggered a public outcry when he proposed a tax hike that would have crushed an already gutted working class, which has been enduring high costs of living around grain and fuel especially. Young people rose up in protest, with widespread support from suffering demographics across the age spectrum. Dozens died in the ensuing, brutal clashes with armed police. Ruto backed away from his tax plan, but the damage was done; the protests continue because the population has no confidence in his ability to put the people first. They want him out, ASAP.

And yes, many local specifics reflect the usual frustrations around government corruption and incompetence. A subsidy supposedly sent to the grain industry never showed up, leading people to ask why they keep getting squeezed for more cash that the government can’t seem to manage responsibly. Kenya is also still recovering from corruption around two failed dam projects, which yielded grave investment losses.

But behind anecdotal incidents of financial mismanagement is a bigger pressure point: the obligations that Kenya owes to the International Monetary Fund (IMF). It’s not that Kenya is a country without means—it has a thriving economy, third to Nigeria and South America in sub-Saharan Africa—but it’s also caught in a typical vice-like arrangement for many struggling countries around the world.

Kenya already owed $2.5 billion to the IMF going into the year, and 68% of its GDP goes to paying off that loan. In 2022, when Ruto first came into power, he scrapped key food and fuel subsidies as a condition of the IMF loan agreement, immediately knocking Kenyans into higher costs of living. The next year, he raised fuel costs in similar deference to an IMF policy recommendation—then met with their ire when reintroducing a subsidy that it claimed could distort the local budget. The country then received a lending boost of some $940 billion this year, and the proposed tax hike was in part a response to the obligations this new burden created.

Kenya is the world’s latest outspoken victim of debt servicing, an issue that UN action groups have been warning about for years. I wrote last year about the 2023 report, but the 2024 version, out in early June, really makes one wonder how much traction exists to do anything about this mounting global problem. Although some improvements exist in this year’s report, they also reflect a natural readjustment after the hard spike of our first years in pandemic; what they do not reflect is redress of our deeper crisis.

Last year, public debt reached $97 trillion USD, growing twice as fast in developing countries as in other parts of the world. Now, debt unto itself can be useful; it can reflect a long-term investment not only in local community growth, but also a web of growing trade relationships with other parts of the world. When countries are in debt to one another, they are also essentially locking themselves into power relationships with one another—and not always in solely the favour of the creditor.

For instance, as much as it’s colloquially feared that China could just “call in” the portion of US debt it lays claim to ($850 billion), the financial world is one big confidence game. If China were to “call in” its debt at a time when the US couldn’t answer it, that would certainly depreciate the US economy—but it would also make China’s holding worthless. And that would have consequences for China’s own creditors and debt relationships. More often than not, then, it’s the gentle “tug” of active debt relationships between major players that keeps other economics thriving.

But therein lies part of the real underlying problem: we’re not dealing with simple trade relationships between states all the time—or even most of the time. For instance, although China holds a significant chunk of US debt, China has also lately been in default on its payments to private US holders of Chinese debt, which has led private lenders in the US to try to pressure their government into calling in this foreign debt for them—irrespective of the broader implications for the rest of the games that states play with one another through direct financing relationships.

And this is where the world’s debt crisis gets super sticky.

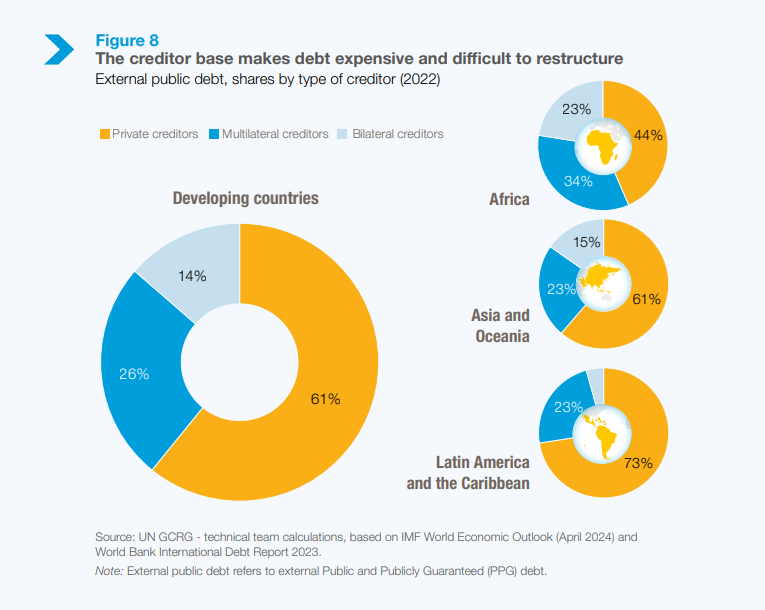

As illustrated in the cheerful pie charts below, from A world in debt 2024: A growing burden to global prosperity, the world is increasingly governed by private creditor relationships. As I noted last November, when writing on Argentina’s situation for now-defunct OnlySky, this situation makes it extremely difficult for countries to renegotiate debt arrangements in response to changing scenarios. In that case:

Argentina underwent two major debt restructuring deals in that decade, but they just created more problems. A deal in 2001 allowed Argentina to pay interest only to those who had opted in to the restructuring plan, and the exclusion of “holdouts” was reasserted after 2010, when the debt plan was agreed upon by 93% of bondholders. The remaining 7% weren’t having this, though: a few hedge fund creditors sued the Argentinian government for breach of a principle of equal treatment for bondholders, pari passu. The South District Court of New York agreed with them, and even though Argentina tried to continue paying its “holdin” creditors, as per the debt restructuring plan, those payments were not permitted until Argentina paid the holdouts, too, in compliance with the court’s rulings.

In the world of finance, these sorts of problems tend to have cascade-failure consequences, so it’s also no wonder that countries struggling to pay back loans to a wide array of differently fickle creditors also find themselves in even worse straits when trying to secure new loans and related investment opportunities.

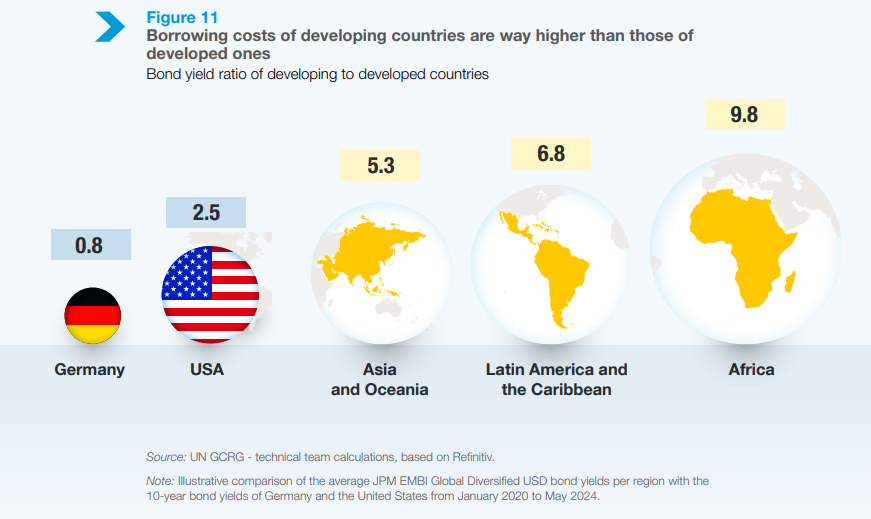

Kenya’s shilling depreciated heavily in recent years, which magnified the amount it owed in US dollars in relation to local currency. Now, as the following graph illustrates, African nations face huge borrowing costs compared to developing nations (a bond yield ratio of 9.8 to the US’s 2.5, for example). This means that even though Kenya is by no means the only country wrestling with a high debt-to-GDP load (e.g., the US hit 121% in 2022), it is one of many countries with very little wiggle-room when trying to negotiate critical terms for new loan arrangements.

And that’s where the austerity measures kick in.

That’s when creditors control a country’s budget, value-scraping everything they can from public services, and stripping any hope of greater investment in local futures.

Foreign countries as creditors are bad enough. The IMF is bad enough. But when you also have to deal with a wide range of private creditors with no real market incentive to play nice, you end up with nightmare scenarios for everyday citizens.

It doesn’t matter if other people screwed up with the start-up costs for local dam projects. It doesn’t matter if government officials lost a grain subsidy along the way.

At the end of the day, everyday human beings who simply want what most of us want—safety and security for their families, and reasonable economic opportunities for personal growth and stability—are left driven to the streets in despair because their governments are too much in the pockets of predatory lenders to be able to manage any further incidents of failure (whether from corruption, project collapse, or unforeseen environmental factors) without wringing them dry.

And that’s really why this matters to us all, whether or not you’re planning on moving to Kenya anytime soon. In the wake of this latest attempted shake-down to pay IMF debts, food costs have again surged in Kenya, which is a net importer of food stuffs—but the system-wide problems with our international loan arrangements have been known for as long as I’ve been alive. They’ve just taken on an added level of urgency as we find ourselves facing massive international problems with so little on-the-ground readiness from every nation around the world to do its part.

This was by design. We value-scraped everything we could get our hands on.

And now, as the world faces harsher consequences from climate crisis, we’re left without the local systems in place to mitigate its impact effectively. Displacement pressures are going to keep rising because of these economic failures. Resource wars will, too—embroiling us in deeper international conflicts shrouded by further “culture war” nonsense that ultimately comes down to more desperate attempts to secure key shipping routes and raw and refined minerals for whatever markets lie ahead.

As Jacobin noted when writing on Kenya’s debt repayment plight in March,

At the start of the 1980s, most African leaders, from elected presidents to dictators, were forced to take out massive IMF and World Bank loans and adhere to the strict neoliberal model that the institutions touted.

To get approval for these loans, the Bretton Woods institutions required leaders to implement “structural adjustment programs” (SAPs). These programs mandated strict austerity and cuts to social spending, while reorienting economies to focus almost entirely on exports and extraction. For most countries, this meant investments into education and health care dried up, while cheaper exports to the West increased.

According to the IMF, this model would boost economic growth and end poverty. It did the opposite.

After structural adjustment programs had been aggressively applied to sub-Saharan Africa, the number of people in poverty almost doubled from 1981 to 2001, “from 164 million to 316 million living below $1 per day,” as noted by the World Bank. According to the Center for Economic and Policy Research, GDP per capita in sub-Saharan Africa fell by 15 percent from 1980 to 1998. Yet, over the previous two decades (1960–1980), prior to the introduction of structural adjustment programs, GDP per capita had increased by 36 percent.

The spread of poverty and the de-development on the continent in the 1980s and the 1990s led to this era being labeled the “Lost Decade.” As early as 1991, the UN secretary general Javier Pérez de Cuéllar pointed to the IMF as one of the leading causes. “The various plans of structural adjustment — which undermine the middle classes; impoverish wage earners; close doors that had begun to open to the basic rights of education, food, housing, medical care; and also disastrously affect employment — often plunge societies, especially young people, into despair.”

As a result of the SAPs, sub-Saharan Africa transferred $229 billion to the West from 1980 to 2004, in the form of debt payments. According to the Canadian Centre for Policy Alternatives, by 2004, the continent was paying the wealthiest countries $15 billion every year in debt servicing. “This is more than the continent [received] in aid, new loans or investment.”

Now, as I’ve noted before, China has a different investment model in Africa. It’s tackling on-the-ground development of core infrastructure (roads, schools, energy) to try to boost African nations into a position to contribute to second-tier competitive market, such as refined mineral production and more elaborate commercial products.

But this approach is not well-liked by many groups in the West—and not just because of the usual sabre-rattling between superpowers. It’s also cutting into a key part of the financial strategy. Direct investment in public infrastructure in the developing world runs at cross-purposes to the austerity measures employed for decades as part of Western “aid”: approaches to “uplift”, that is, which prioritize keeping other countries in a position of dependency on global markets, to refine whatever raw materials can be pressured out of their territory in the form of immediate exports to pay off debts.

It’s an ugly business, realizing just how much the West’s current state of affluence—precarious though it is as well—has relied on predatory financial relationships: both directly, through major state-driven and internationally sanctioned bank programs, and indirectly, through financial systems that invite private actors to gouge away, too.

But it’s also a reckoning we’d better be ready for, as the consequences of an unchecked world of debt servicing amplifies our collective problems—for migration, for climate change mitigation, for energy futures, and for any hope of minimizing resource wars. Between the IMF’s failures and the surging realm of predatory private creditors, we’re not just left with breaking points like Kenya’s latest round of anti-austerity protests.

World events like this are a litmus test for global readiness to commit to genuine human development over the easily manipulated abstractions of GDP growth.

How do you think that test is playing out?

Be well, be kind, and seek justice where you can.

ML

it's always time to shear the sheep in some part of the world, isn't it? great assets, going cheap. our turn was 2007, of course. relentless concentration of power and wealth to the elites has to give at some point. one would hope …

As you so compellingly and painstakingly point out (a word my brain has habitually cleaved into “ pain-staking” rather than the correct “ pains-taking”), that goddam test is not going well, and it is not going to go well.

Humanity did not, cannot, and will not get off the “treadmill of production” that Schnaiberg/Gould delineated (albeit with copious 60s style We-Shall-Overcome hopium) in their Environment and Society books of the early 90s.

And that’s where I’m staking my pain of the world.

The light of the world? People that know this shit.